The payments landscape has shifted dramatically over the past two decades. What once functioned as a purely operational backend—meant to move money and nothing more—has evolved into a critical decision-making layer for modern businesses.

This transformation didn’t happen overnight. It unfolded in clear, distinct stages: starting with rigid infrastructure, moving into modular orchestration, and now entering a new era powered by agentic intelligence. Understanding this evolution isn’t just useful—it’s essential for merchants building modern payment strategies.

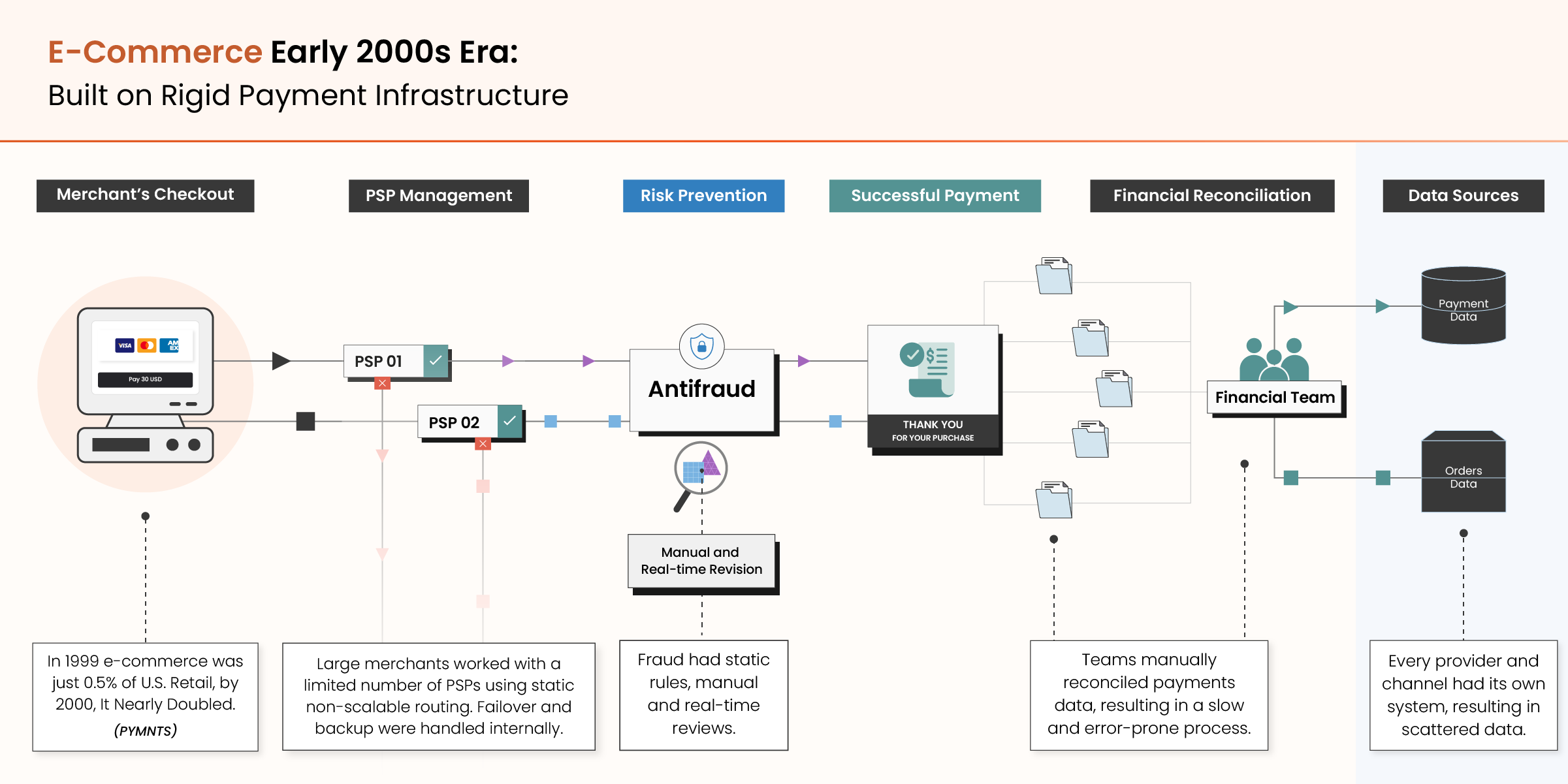

In the early stages of digital commerce, payment infrastructure was built for stability, not flexibility. Merchants typically worked with a single PSP, fraud was handled through basic rules, and reconciliation took days—if not weeks.

Key limitations of this model included:

The outcome? Payments worked, but only in a narrow sense. Every failed transaction meant lost revenue, and there was little merchants could do to recover or respond in real time. Payments were operational, not strategic.

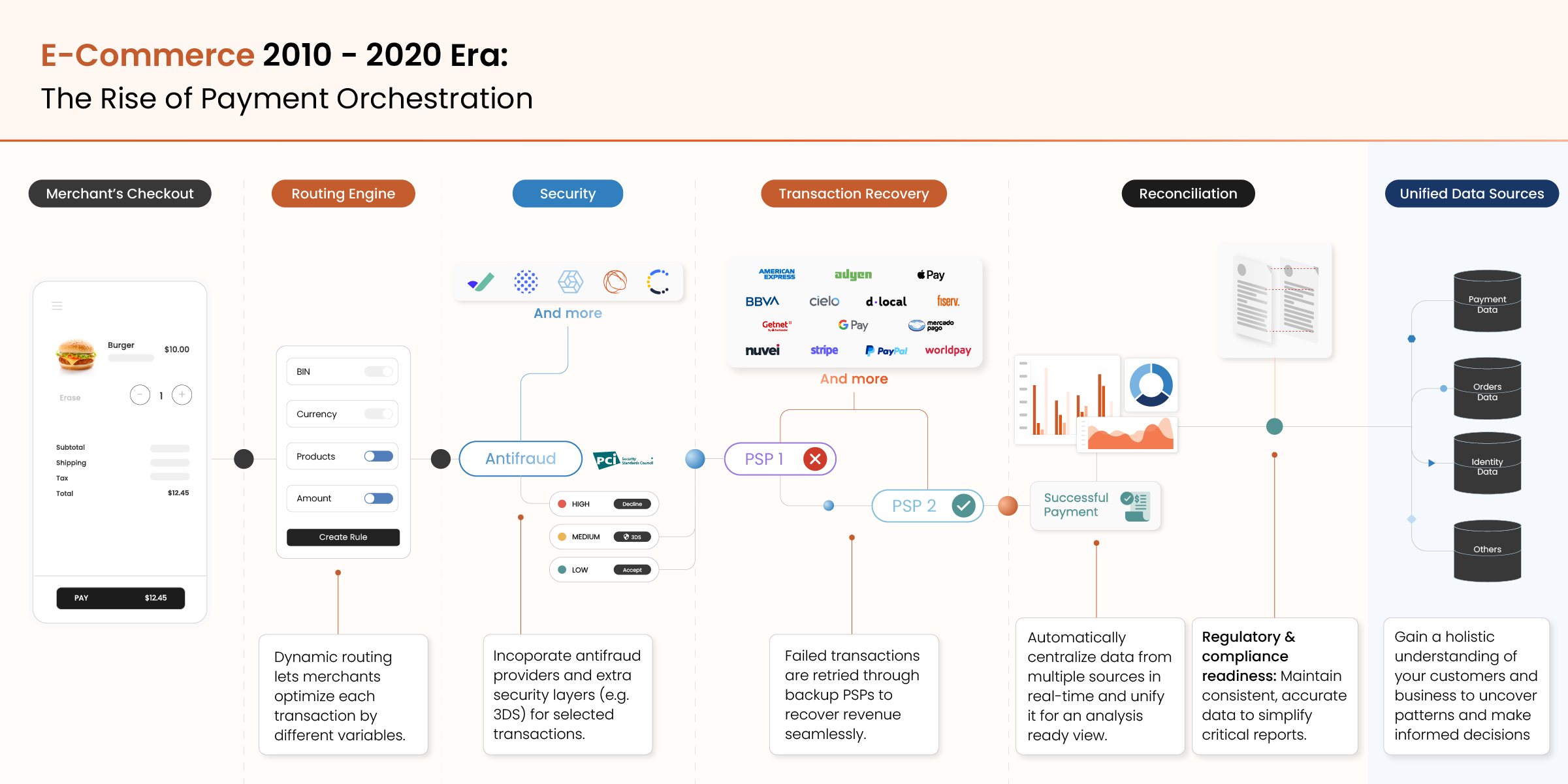

As global expansion and digital scale became priorities, a new layer emerged—payment orchestration. This decoupled payment logic from providers, allowing businesses to dynamically route transactions, recover failures automatically, and centralize control.

Key breakthroughs included:

With these capabilities, merchants saw a marked improvement in approval rates, cost efficiency, and time to market. More importantly, they began to treat payments as a lever for growth.

But orchestration still depended on predefined logic. Teams had to set the rules, monitor performance, and interpret dashboards manually. The system was smarter—but not yet autonomous.

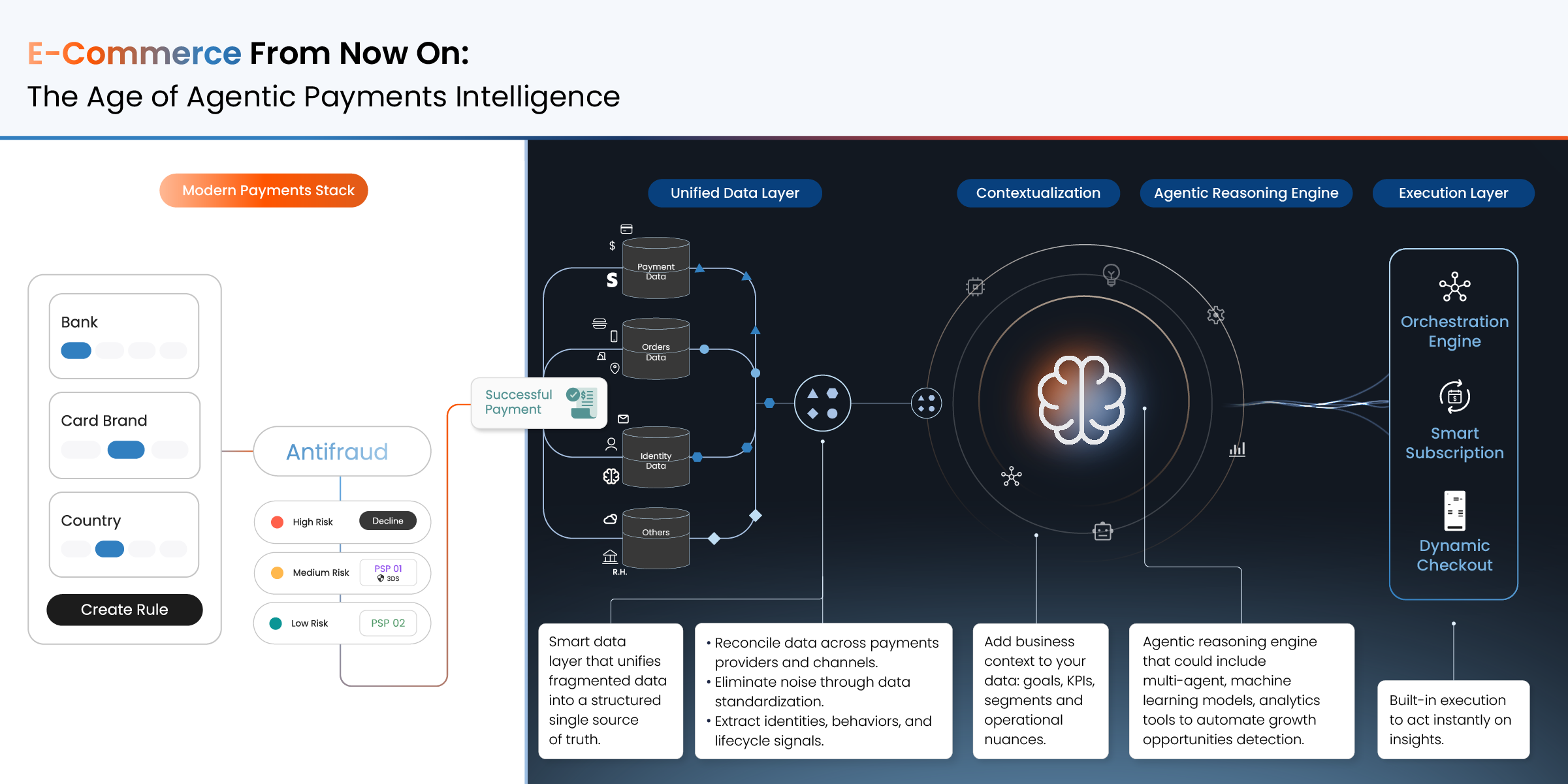

Today, we’re entering a new phase. One where payments infrastructure isn’t just programmable—it’s intelligent. This is the era of agentic payments intelligence, where systems reason, decide, and act without waiting for human intervention.

The core difference lies in agency: the ability of the system to not only process data, but understand context and execute autonomously.

Agentic platforms are designed to resolve the most persistent pain points in payments—challenges that even orchestration layers haven’t fully solved:

Merchants often rely on multiple PSPs, fraud solutions, and checkout platforms—each with its own data silo. This slows decision-making and hides key growth blockers like approval rate drops or fraud spikes.

Agentic systems bring unified analytics across all sources, providing real-time dashboards and insights for finance, operations, and growth teams. More importantly, they act on those insights through predictive, AI-assisted decision-making.

Even with orchestration, many merchants routing logic or switch PSPs. When approval rates drop in a specific region or a provider begins underperforming, it may take days—or weeks—to react.

Agentic systems eliminate that lag. They apply smarter routing, detect patterns in approval performance, cost, and latency, and automatically reroute traffic based on what will drive the best outcome. There’s no need to submit tickets or wait for deployment. The system adapts in real time—ensuring that payment orchestration becomes not just modular, but intelligent.

Local payment methods (APMs) are essential for conversion in global markets. But integrating, tracking, and optimizing them still requires manual effort and engineering time. Worse, performance by region often goes unmonitored, leading to lower conversion and lost revenue.

Agentic platforms continuously assess APM performance by region, channel, and user type. If a preferred payment method underperforms—or is missing entirely—they can recommend or even deploy alternatives autonomously. That means better coverage of local payment preferences and a truly expansion-ready payments stack.

Fraud is dynamic, but most systems aren’t. Traditional fraud prevention still relies on static thresholds and batch updates, forcing teams to choose between overprotection (which kills conversion) or underprotection (which leaks revenue). Manual chargeback workflows create additional overhead.

Agentic fraud engines apply real-time fraud insights and adaptable logic that evolves with every signal—adjusting thresholds per region, user behavior, and risk profile. They also automate chargeback responses, reducing operational burden while preserving trust and compliance.

Recurring and subscription businesses often lose revenue to silent churn caused by failed payment attempts. Most retry systems operate on simple rules: retry at fixed intervals regardless of context.

Agentic retry engines go further. They analyze historical success patterns, customer behavior, and payment method performance to determine when and how to retry for maximum recovery. They continuously learn and improve, minimizing churn while boosting retention.

Looking at this shift holistically, it becomes clear:

This is not just a technological progression—it’s a shift in how businesses operate. Payments are no longer just a cost center. When driven by agentic systems, they become a strategic decision engine capable of influencing revenue, retention, expansion, and resilience.

Today’s payments leaders are not just optimizing—they’re anticipating. They’re moving beyond dashboards and rules toward systems that can reason, act, and learn at scale.

Agentic payments intelligence makes this possible. It transforms payments from infrastructure into strategy—handling complexity not as a burden, but as an opportunity to outperform.

For companies that want to grow globally, operate efficiently, and stay ahead of risk, agentic systems aren’t a future investment—they’re a present advantage.

Because in the next era of commerce, execution alone won’t be enough.

Intelligence will win.