For the past 18 months, the agentic commerce industry has been running a fragmented race. Google launched its Universal Commerce Protocol. OpenAI and Stripe co-authored the Agentic Commerce Protocol. Mastercard built direct integrations with AI platforms. Visa introduced its own Trusted Agent Protocol. Every major player was betting on their own standard, and merchants were left watching, unsure which protocol to integrate with, and aware that betting on the wrong one could mean rebuilding their stack when the dust settled.

On April 8, 2026, Visa made a move worth paying attention to.

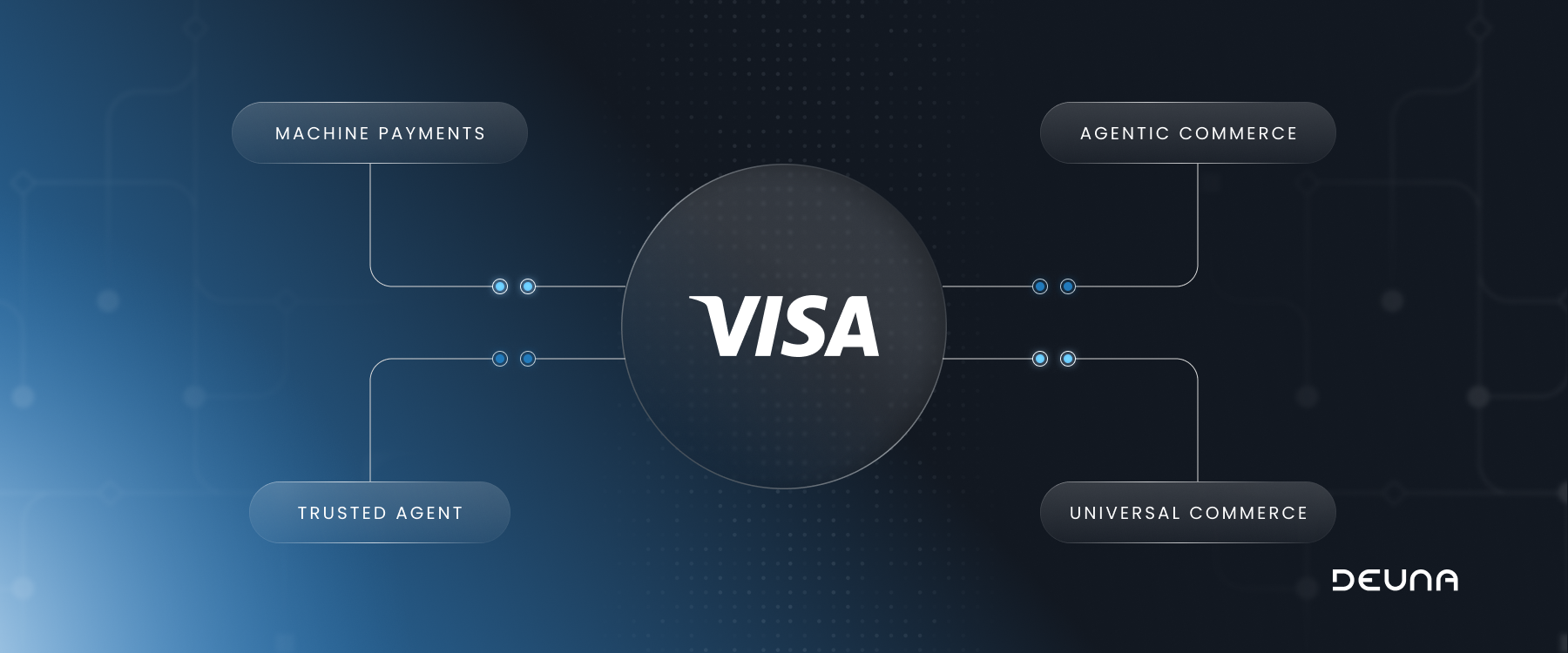

Visa's Intelligent Commerce Connect acts as a network, protocol, and token vault-agnostic entry point to agentic commerce for agent builders, merchants, and enablers, enabling merchants to accept payments initiated via the four major agent protocols: Trusted Agent Protocol, Machine Payments Protocol, Agentic Commerce Protocol, and Universal Commerce Protocol.

In other words, Visa built a layer that connects to multiple protocols simultaneously, rather than pushing its own standard as the single answer. By supporting all four protocols, Visa is positioning itself as the neutral payment layer underneath that competition, ensuring that no matter which protocol dominates, agentic transactions still flow through its network.

This is not a minor product launch. It is a strategic repositioning that changes what the protocol question actually means for merchants.

The protocol landscape between Google, OpenAI, Mastercard, and others is still very much active. No single standard has won. The question now shifts from which protocol wins to who controls the gateway routing them all.

For merchants, this changes the calculus significantly. The question is no longer "which protocol should we bet on?" The question is "do we integrate directly with each protocol, or do we integrate with a layer that handles all of them?"

The merchants who integrate directly with individual protocols are making a bet on which ones will dominate. That bet may pay off. But it also means rebuilding or extending integrations as the protocol landscape shifts, and it is still shifting. Visa is framing the market problem as integration complexity across networks, protocols, token vaults, merchant systems, and AI shopping surfaces. Intelligent Commerce Connect is their answer to that complexity. A single integration point that works regardless of which protocol an AI agent is running on.

The merchants best positioned to capture agentic commerce volume are not the ones who picked the right protocol. They are the ones whose infrastructure can handle any protocol without requiring a custom integration for each one.

Intelligent Commerce Connect integrates Visa's APIs alongside other payment network APIs, allowing agents to pay with both Visa and non-Visa cards, giving businesses more choice while supporting ecosystem-wide adoption of agentic payments. That multi-network support is significant. It means the infrastructure is designed not to lock merchants into Visa's ecosystem, but to operate as a neutral layer across the broader payment landscape.

The parallel to traditional payment orchestration is direct. The merchants who solved multi-PSP complexity by adding an orchestration layer above individual processors are the ones who adapted fastest when the provider landscape changed. The merchants who built direct point-to-point integrations had to rebuild every time something shifted.

Agentic commerce is presenting the same choice, at a faster pace.

The merchants who will capture early agentic commerce volume are not the ones who picked the right protocol. They are the ones who built infrastructure flexible enough to work with any of them.

DEUNA's orchestration platform is designed precisely for that kind of adaptability.

Rather than requiring merchants to bet on a single integration path, it provides a unified layer that connects to providers and protocols as they evolve, without rebuilding the stack every time the landscape shifts. In a market where the protocol question is still being answered, that flexibility is not a feature. It is the foundation of a durable payments strategy.