These three terms get used interchangeably in vendor conversations, RFPs, and board presentations. They are not the same thing. And the confusion between them leads to infrastructure decisions that cost enterprises millions in missed optimization, excessive fees, and operational drag.

Here is what each one actually does, when you need it, and why the difference matters at scale.

Its job is to securely transmit payment data from your checkout to a bank or processor. It tokenizes card information, sends the authorization request, and returns an approval or decline. A payment gateway is a static service: the payment methods are presented in the same way under all circumstances, the route to the acquirer is fixed, and all transactions go to the same destination.

If your primary acquirer goes down, a gateway does not automatically reroute. If one processor performs better for a specific card type or geography, the gateway does not know or care. It moves data from point A to point B. That is its entire function.

For a merchant operating in one market with one processor, a gateway is sufficient. For anyone operating at scale, it is a starting point, not a strategy.

A Payment Service Provider gives you the technical connection of a gateway, plus additional services like acquiring relationships, fraud tools, settlement, and compliance management, all packaged under one contract. PSPs connect directly to acquiring banks, card networks, and local payment schemes, consolidating authorization, clearing, settlement, merchant onboarding, and fraud checks into a single platform.

The value of a PSP is simplicity. One contract, one integration, one point of contact. For merchants earlier in their growth, that simplicity is worth the trade-off. The trade-off is dependency. Your performance is entirely determined by how well that one provider handles your transaction mix, in your markets, for your customer base. When it underperforms, you have no alternative and no visibility into why.

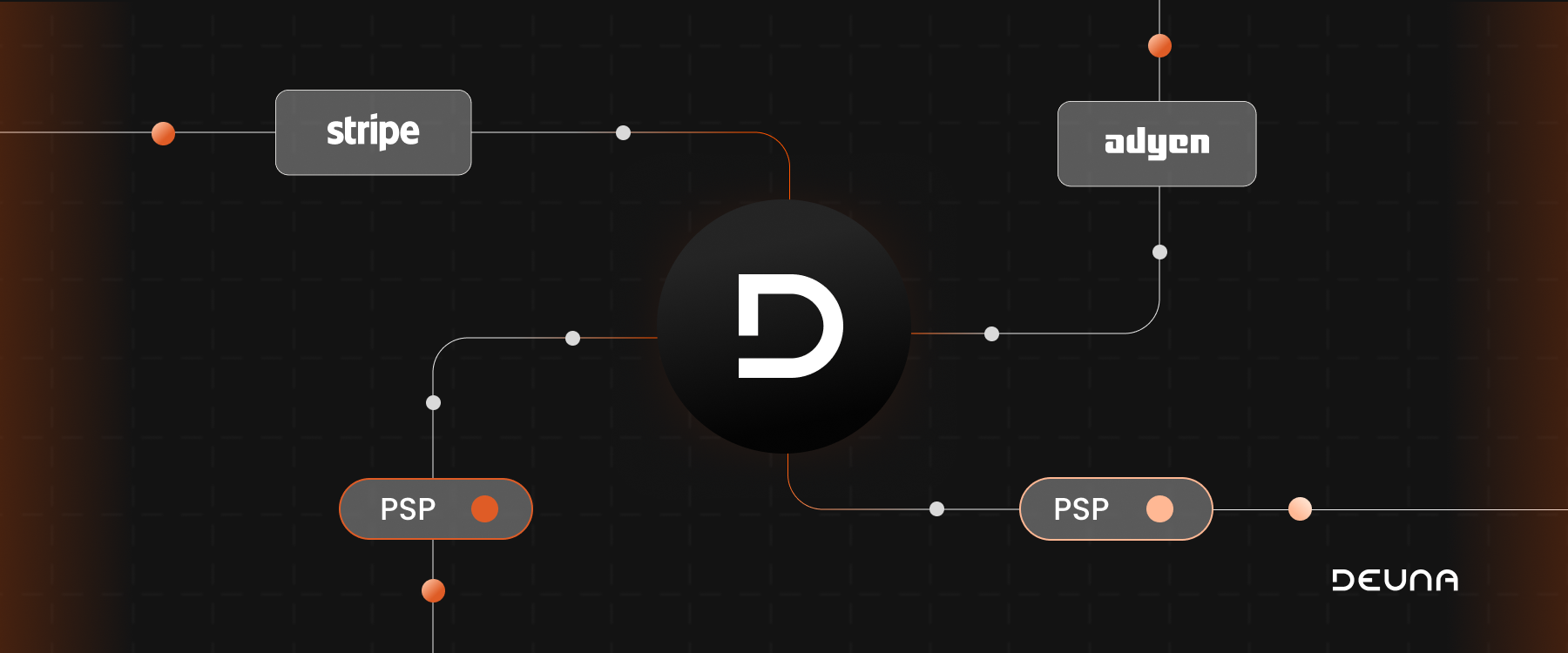

Payment orchestration is a technology layer that connects a business to multiple PSPs, gateways, and acquirers through a single integration. It applies smart routing, failover logic, and centralized analytics to improve payment performance, reduce costs, and expand coverage across regions.

The orchestrator does not process payments. It decides who should. It evaluates each transaction in real time and routes it to the provider most likely to approve it, at the lowest cost, given the card type, geography, amount, and risk profile. When a provider goes down or underperforms, it reroutes automatically. When you want to add a new provider for a specific market, you do it once in the orchestration layer without touching your checkout or your existing integrations.

This is the critical distinction: a payment gateway is at the foundation of a payment orchestration platform, but it is just one element. The orchestrator manages the entire ecosystem above that foundation.

A gateway alone makes sense when the complexity and scale of your business does not yet justify investing in multiple solutions. If your transaction volume is manageable, your payment mix is straightforward, and a single provider relationship covers your needs without meaningful performance trade-offs, the added cost and maintenance overhead of a more sophisticated setup is not warranted.

A PSP makes sense when you need more than a technical connection. When compliance, fraud management, and settlement need to be handled under one roof and your business is growing but has not yet reached the point where the limitations of a single provider are costing you meaningful revenue, a PSP gives you the breadth of services you need without the complexity of managing multiple integrations.

A payment orchestrator makes sense when the scale and complexity of your business has outgrown what any single provider can optimize. When your transaction mix spans multiple card types, geographies, and customer segments, when provider performance varies enough to have a measurable impact on your approval rates and costs, or when your team is spending more time maintaining your payment setup than improving it, orchestration is not an upgrade. It is a structural requirement.

The infrastructure layer you choose today determines your optionality tomorrow. Merchants locked into a single PSP cannot capture the performance gains that come from intelligent routing across providers. They cannot negotiate from a position of strength because switching costs are high. And they cannot respond quickly when a provider underperforms, because there is nothing to fall back on.

The gateway moves your transactions. The PSP bundles the services around them. The orchestrator is what makes every layer of that stack work together intelligently, giving you the control, visibility, and flexibility to optimize performance across every market, provider, and transaction profile you operate in.

For enterprise merchants, that control is the difference between a payment stack that processes and one that performs. DEUNA was built for the latter. A single integration to 400+ providers, with the orchestration logic and intelligence layer to make every transaction decision count.