Most checkouts were designed to display payment methods, not to choose them.

There's a difference. A big one.

When a merchant integrates Apple Pay, PIX, credit card, and BNPL into their checkout, they usually configure a static order: card first, wallets second, installments at the bottom. That order stays the same for every user, every device, every transaction size, every market.

The logic behind it? "We offer options. The user will pick what they want."

That logic is costing you more than you think.

In 2024, 61% of consumers abandoned a purchase because their preferred payment method wasn't offered, or wasn't visible enough.

That second part matters.

Not unavailable. Not unsupported. Just not surfaced correctly.

That's not a product catalog problem. That's a presentation problem, and a personalization problem.

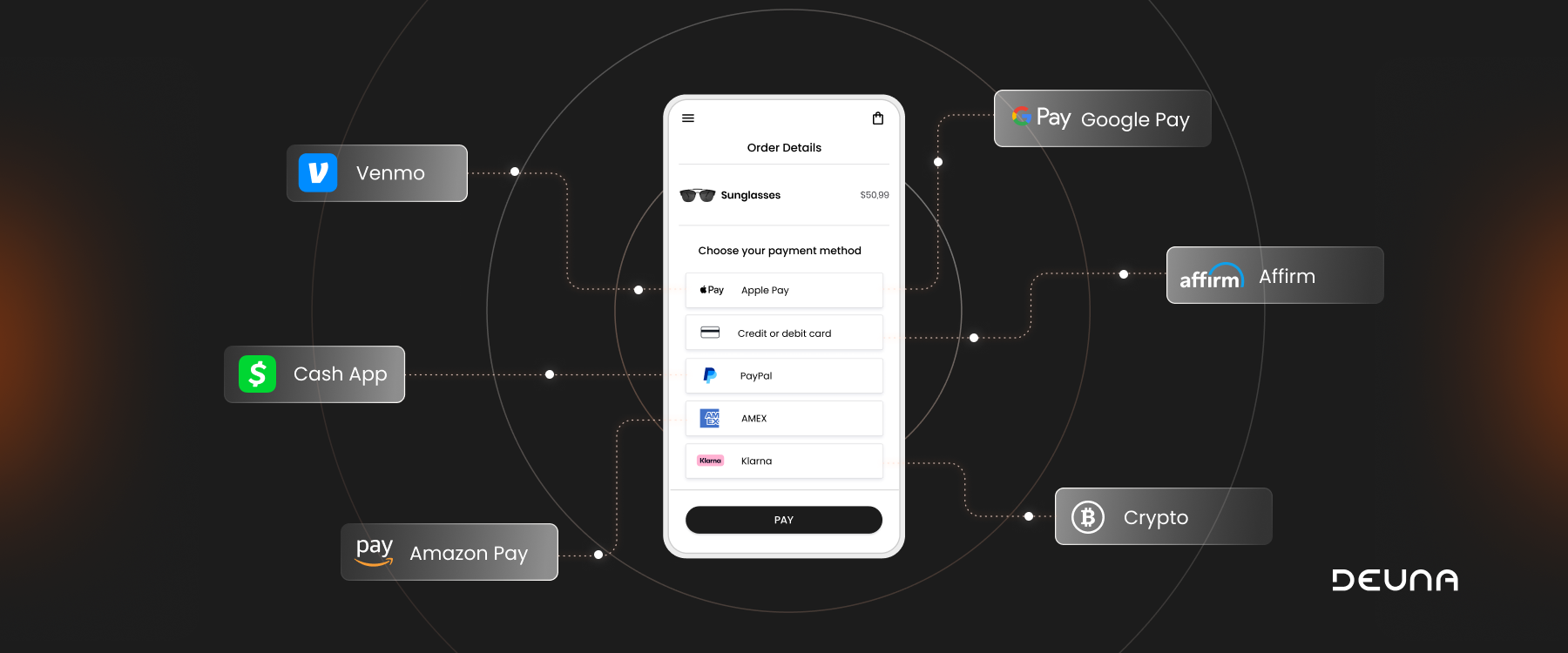

Adding a single relevant payment method increases conversion by an average of 7%. The top three preferred methods in a given market can improve conversions by up to 30%. But "relevant" is doing all the work in that sentence. Relevant to whom? In what context? At what point in the session?

Static checkout configurations can't answer those questions. They were never designed to.

It's not AI for the sake of AI. It's a specific idea: show the right payment method, to the right shopper, at the right moment.

That means the checkout reads context (device, location, purchase amount, user history, authentication state, time of day, merchant category) and uses that to rank, surface, or highlight the option most likely to convert for this specific session.

It's not about removing options. It's about reducing cognitive load at the most critical second of the entire purchase journey.

A user on mobile, buying a pizza, coming from a repeat session and already authenticated, should see their saved payment method front and center. Not a card form.

A new user with a high-value ticket, on a first visit from an unknown device, probably needs trust signals and familiarity more than speed. Show them the method they recognize from their banking context.

Same merchant. Same checkout. Completely different optimal experience.

Users with saved cards convert at 83%. Users without saved cards convert at 75%.

That 8-point gap sounds modest. Multiply it by millions of transactions across an airline, a quick service restaurant chain, or a cinema network, and it becomes a number that justifies serious engineering investment.

But here's the part most teams miss: saving a card is not the only thing driving the difference. Recognition drives the difference. The user feels known. The friction of starting from scratch disappears. The checkout adapts to who they are.

Smart checkout is, at its core, a recognition system that happens to have payment opinions.

The context that should inform a checkout isn't only what happens inside the checkout.

It's what happened before: the channel the user came from, whether they're on a native app or a mobile web session, whether this is their first device or their usual one, whether they started a cart yesterday and came back today.

A user who clicked from a WhatsApp payment link behaves differently than a user who searched and landed organically. A user on iOS Safari has different wallet availability than a user on Android Chrome.

Adaptive checkout means reading all of those signals, not just the ones that happen inside your widget.

The checkout that converts is the one that feels like it already knew you were coming.

Every time a user has to scroll past four irrelevant payment methods to find their preferred one, you're paying a tax.

Every time your checkout shows the same options to a first-time mobile user and a VIP returning desktop user, you're paying a tax.

Every time your payment method order was set in a Jira ticket two years ago and nobody has questioned it since, you're paying a tax.

That tax doesn't appear as a line item. It appears as your conversion rate is 2 points lower than it should be. As your APM adoption underperforms despite the integration effort. As your returning user experience feels just as generic as your new user experience.

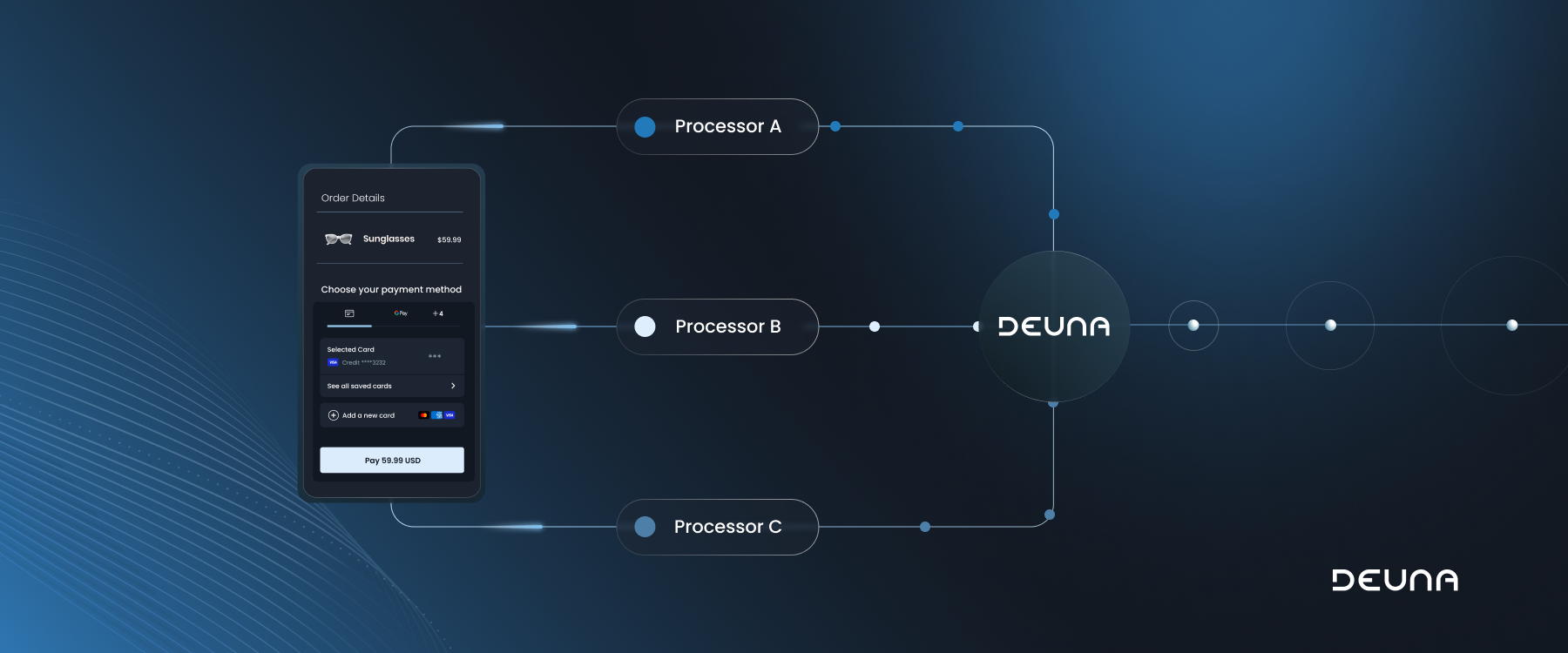

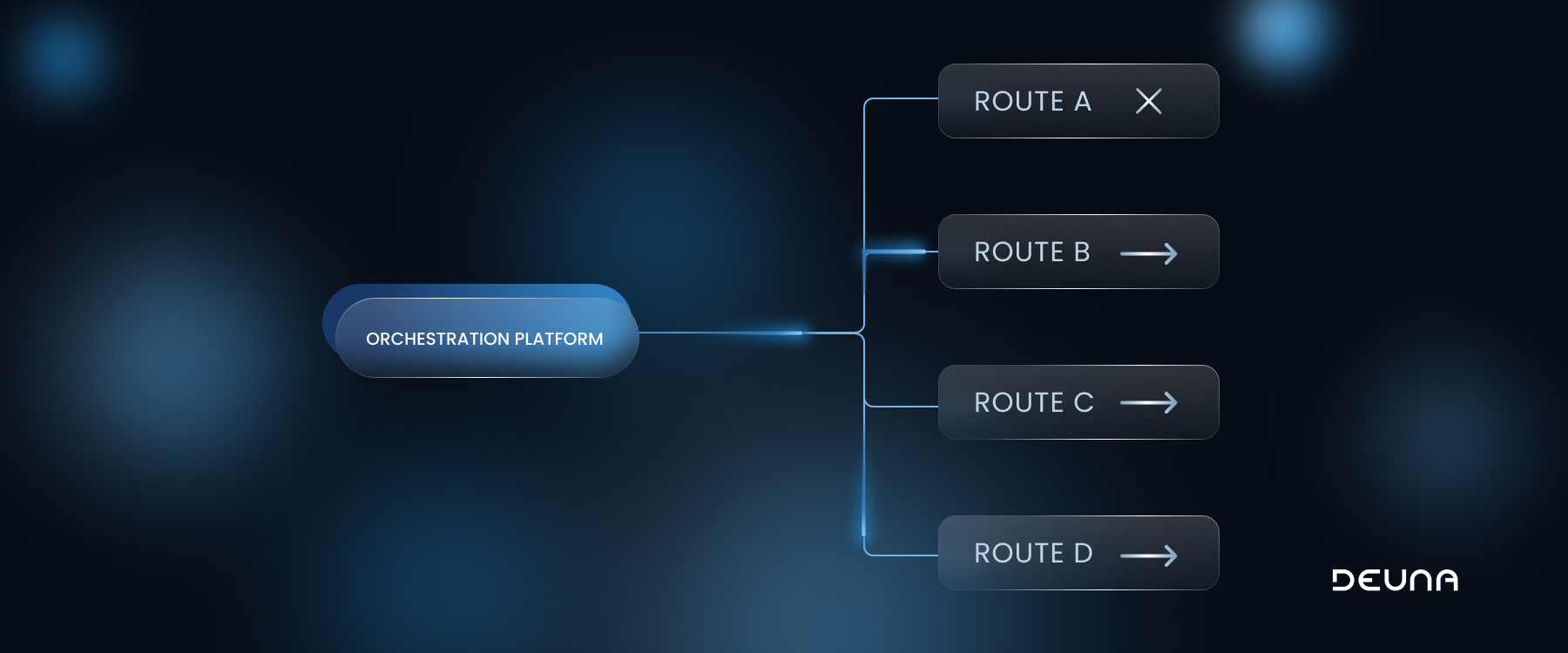

Let's be specific about what AI does here, because "AI-powered checkout" has become noise.

What actually works today:

What's emerging:

The companies that will win in agentic commerce aren't the ones with the most payment methods. They're the ones whose checkout can communicate payment preferences programmatically, to a system that never sees the UI at all.

The checkout that adapts isn't a future product. The signals to build it exist in your transaction data today.

The question is whether your checkout is listening.