As digital commerce continues to scale, payments have become one of the most critical drivers of revenue. Even small inefficiencies in payment performance can translate into measurable financial impact. For a business processing $1 billion in annual transactions, a 1% increase in authorization rate equals $10 million in recovered revenue — without acquiring new customers, increasing marketing spend, or changing pricing. At scale, optimizing how payments are routed is one of the highest-leverage levers available to enterprise merchants.

At the same time, the cost of processing payments continues to rise. In the United States, total card processing fees reached $198.25 billion between 2024 and 2025, according to the Merchants Payments Coalition . This makes every transaction decision relevant not only for conversion, but also for margin.

For merchants operating with multiple payment providers, routing decisions are no longer purely operational. They directly impact revenue performance, cost structure, and scalability.

Payment routing is the process of directing each transaction to the most suitable payment processor or acquirer within a multi-provider network.

The core insight is this: the same transaction can yield very different approval outcomes depending on which processor handles it. Each acquirer has distinct issuer relationships, authorization logic, and performance profiles across card types, geographies, and transaction categories. Most declines are not caused by the customer. They are caused by issuer behavior, routing inefficiencies, or processor performance. Matching each transaction to the right processor is what separates a high-performing payment stack from one that silently leaks revenue.

In modern payment infrastructures, routing is a strategic lever that directly influences authorization rates, processing costs, fraud exposure, and overall payment performance.

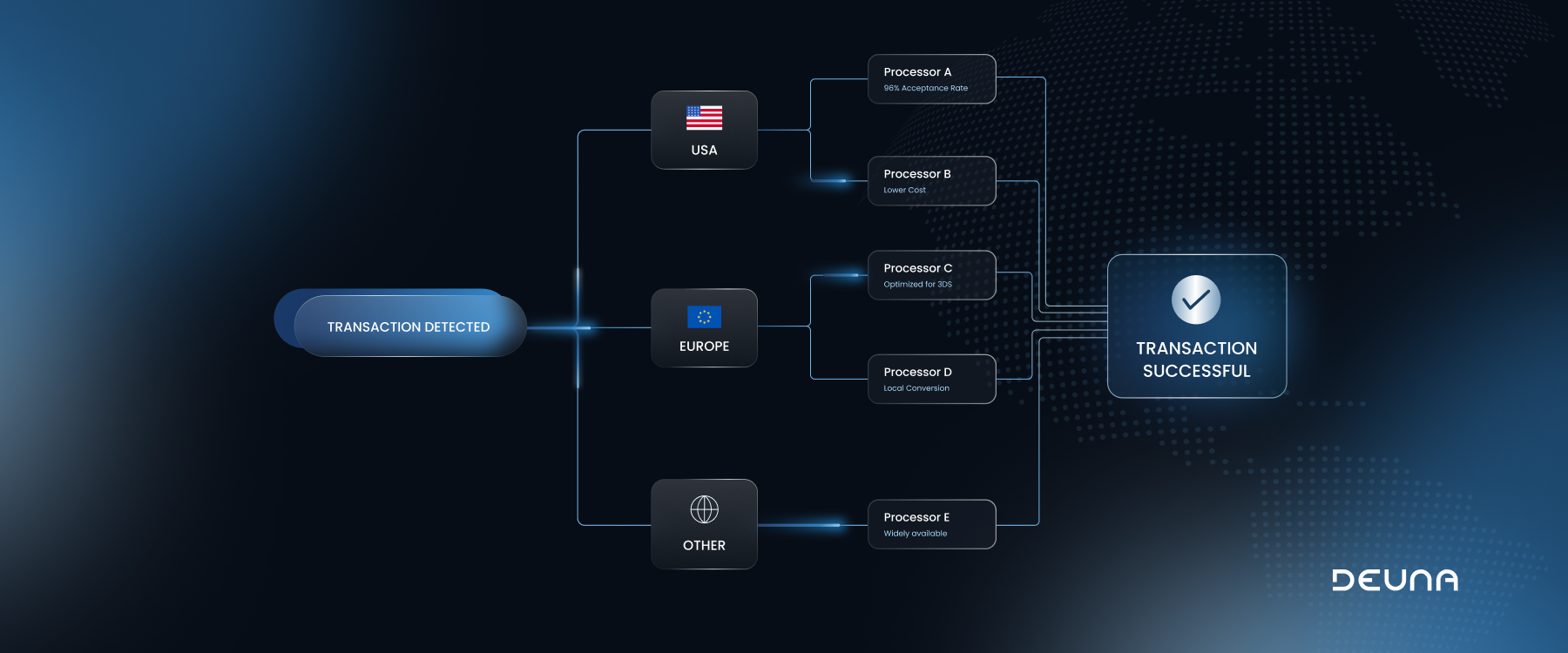

When a customer initiates a payment, multiple variables are evaluated: the issuing bank, payment method, transaction value, and location.

How that information is used depends on the type of routing in place. In manual routing, merchants define fixed rules in advance, for example, always sending transactions from a specific country through a designated processor. It works, but it doesn't adapt. In smart routing, those same variables are evaluated in real time to dynamically select the provider most likely to approve the transaction, optimizing for both performance and cost with every decision.

When a transaction fails due to a temporary issue, a smart routing system can automatically retry through an alternative provider, recovering revenue that would otherwise be lost without adding any friction to the user experience.

For merchants operating at scale, dynamic payment routing provides a clear advantage. It allows continuous improvement, while static routing often results in missed revenue opportunities and inconsistent performance.

The US market has two routing dynamics worth understanding specifically.

The first is PINless debit routing. Following the Federal Reserve's 2022 amendments to Regulation II, issuers must enable at least two unaffiliated networks for all debit transactions, including card-not-present. This gives merchants the ability to route debit across multiple networks in e-commerce environments, and according to CMSPI, least-cost debit routing can generate billions in annual savings for US merchants. Capturing that value, however, requires routing logic that can identify eligible transactions and act on them in real time.

The second is network tokenization. According to Visa, in 2024 the network saw a 44% surge year-over-year in token adoption, translating into a 6% improvement in approvals and a 30% reduction in fraud. Visaacceptance According to Fiserv, merchants transacting with network tokens see an average 2.1% authorization uplift over standard PAN-based transactions, with fraud rates declining by an average of 26%. Fiserv

Both optimizations require the same thing: routing intelligence that operates at the transaction level, in real time. That is what a payment orchestration platform like DEUNA is built to enable.

Payment routing is also a key driver of cost efficiency, especially in high-volume environments where small differences in processing fees have a direct impact on margins.

Different payment processors apply different pricing structures depending on factors such as card network, transaction type, geography, and interchange qualification. Routing allows merchants to actively manage these variables instead of passively accepting default costs.

One practical strategy is routing transactions to optimize interchange qualification. For example, ensuring that transactions are processed through providers that support enhanced data submission or local acquiring can reduce interchange fees and improve net cost per transaction.

Another lever is geographic routing. For cross-border transactions, routing payments through local acquirers in the same region as the issuing bank can reduce cross-border fees while also improving approval rates. This is particularly relevant for US merchants processing international payments.

Merchants can also differentiate routing strategies based on payment method. Debit cards, for instance, often have lower processing costs than credit cards when routed through specific networks. Aligning routing logic with these differences can generate meaningful savings at scale.

Over time, these optimizations compound. In high-volume businesses, even a few basis points of cost reduction per transaction can translate into significant margin improvements without negatively impacting conversion.

As payment ecosystems become more complex, payment routing moves beyond simple transaction distribution and becomes a core driver of performance.

Merchants are no longer just deciding where to send transactions, but how to continuously improve outcomes across approval rates, cost, and reliability. This requires routing systems that can incorporate real-time data, adapt to changing issuer behavior, and respond dynamically to performance signals.

In practice, this means combining routing logic with continuous feedback loops. Approval rates, decline reasons, latency, and cost data all become inputs that inform how future transactions are routed. Over time, this creates a system that improves with every transaction processed.

For merchants operating across multiple providers and markets, this approach allows routing to scale effectively without increasing operational complexity. Instead of manually updating rules, the system continuously adjusts to maintain optimal performance.

At DEUNA, payment routing is not treated as a static set of rules, but as part of a broader system designed to optimize performance across every transaction. By combining payment orchestration with real-time decisioning, DEUNA enables merchants to dynamically route payments based on approval probability, cost, and context.

The result is a more adaptive payment infrastructure that improves approval rates, reduces unnecessary costs, and minimizes failed transactions without adding operational complexity.

Because in today’s payments landscape, success is no longer defined by access to multiple providers. It is defined by how intelligently you use them.