Enterprise payment stacks rarely emerge from deliberate design. They evolve over time.

As merchants expand across geographies and channels, they layer in multiple Payment Service Providers (PSPs), local acquirers, fraud tools, and region-specific solutions. What begins as a strategy for redundancy and coverage gradually turns into a fragmented ecosystem—one where data, logic, and decision-making are distributed across systems that were never meant to work as a whole.

This fragmentation is not just an operational inconvenience. It creates a structural limitation: the inability to generate and act on intelligence at scale.

Because in payments, the problem is not the absence of data. It is the absence of coherence.

A decline in one region may be linked to a new routing configuration that was not even intended to affect the region. A drop in approval rates may correlate with changes in issuer behavior for a specific BIN range. Fraud decisions may conflict with customer-level patterns observed in other channels. These relationships exist—but without a unified view, they remain invisible.

As a result, optimization efforts become localized, reactive, and ultimately capped.

The shift is not simply about adopting new tools. It is about rethinking the architecture of the payment stack.

Orchestration has already addressed a critical first step: connectivity. It enables merchants to integrate multiple providers into a single operational flow and reduces dependency on any single PSP.

However, connectivity alone does not create intelligence.

The real transformation begins when merchants move from connected systems to unified data structures—a foundation that allows AI and machine learning models to operate effectively.

AI does not fail in payments due to lack of sophistication. It fails because the underlying data is inconsistent, incomplete, or misaligned.

Without standardization, models operate on fragmented signals and produce limited or unreliable outcomes. With a unified foundation, those same models can identify patterns, generate insights, and drive decisions with precision.

This is the point where payments transition from a cost center to a performance lever.

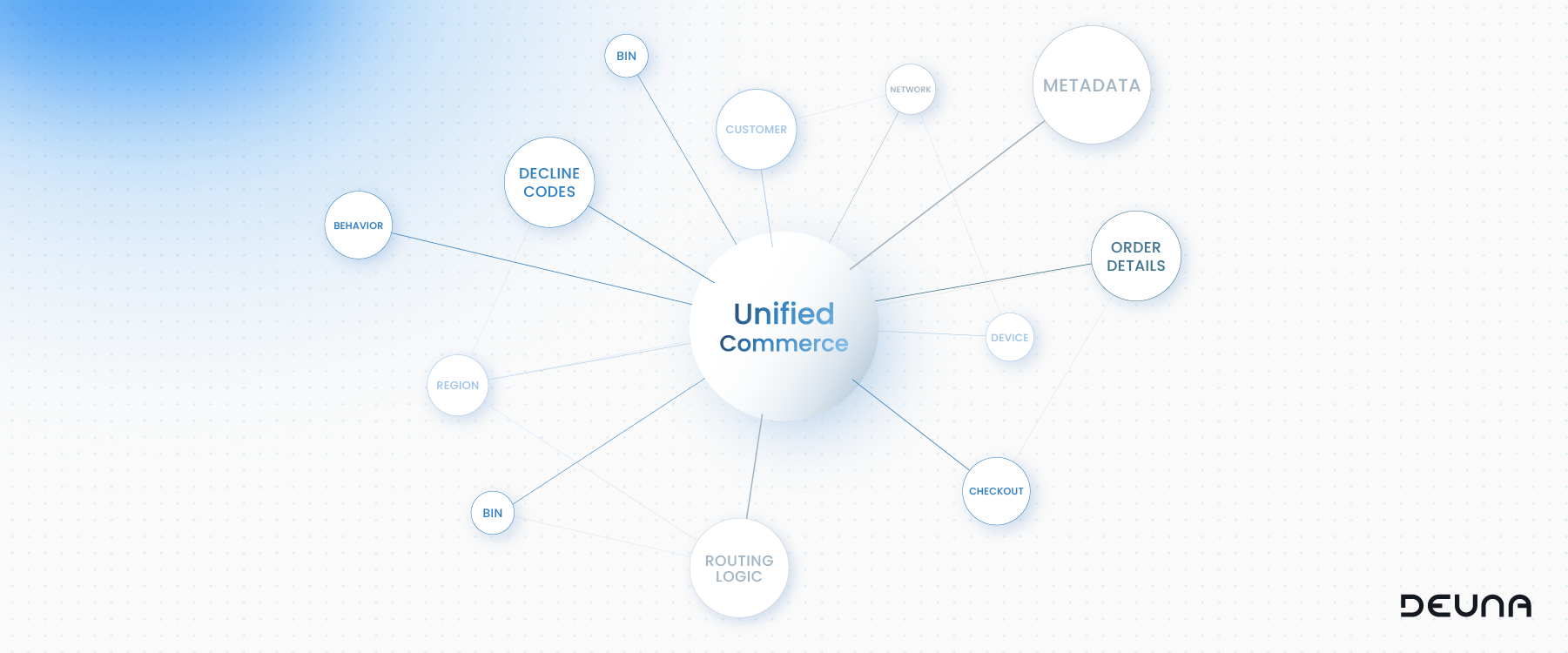

To power payments with AI, merchants must first solve the data integrity problem at its core. This requires more than aggregating data—it requires structuring it.

A unified commerce ontology standardizes every relevant signal across the payment lifecycle:

Instead of disparate logs and provider-specific formats, the system produces a consistent, high-fidelity dataset.

This standardization is what enables machine learning models to operate at scale. Rather than interpreting inconsistent inputs, the system works with a clean, comparable stream of information—turning raw transactions into actionable intelligence.

Traditional systems focus on whether a transaction was approved or declined.

Advanced systems focus on why.

They enrich transaction data with contextual signals, including:

This enables more granular analysis and, critically, the detection of hidden inefficiencies.

For example, what appears as a stable overall approval rate may mask a significant decline within a specific BIN range or issuer segment. Identifying and addressing these micro-patterns is where meaningful performance gains are realized.

Rule-based systems were effective in simpler environments but struggle to scale with increasing complexity.

Static logic—such as predefined routing sequences or retry rules—cannot account for the dynamic nature of issuer behavior, regional differences, and transaction-level variability.

MLs applied to payments introduce a different paradigm. Instead of following fixed rules, they evaluate each transaction in real time, considering:

Based on this evaluation, the system determines the optimal configuration for each transaction and continuously updates its decisions as new data becomes available.

Insights only create value when they are acted on—and in most payment stacks, that’s where the system breaks.

Teams identify issues, but execution requires manual changes, coordination across systems, and deployment cycles. By the time action is taken, conditions have already shifted. Optimization becomes reactive, slow, and inconsistent.

AI-driven architectures remove this gap by embedding execution directly into the transaction flow.

At the core, the system continuously:

And critically, it executes those decisions in real time:

This closes the loop entirely. There is no separation between analysis and action. No delay between insight and implementation. No reliance on manual intervention.

The system doesn’t just inform decisions—it makes and executes them continuously, at transaction level. This is the shift from managing payments to operating an autonomous performance engine.

AI in payments isn’t about better models—it’s about readiness: merchants that remain fragmented will see limited impact, while those that unify data, decisioning, and execution will transform payments into a scalable, continuously optimizing growth engine that compounds performance over time