For a business processing $1 billion in annual transactions, a 1% increase in authorization rate equals $10 million in recovered revenue, without acquiring new customers, increasing marketing spend, or changing pricing.

That is why smart payment routing has stopped being a back-office setting and become a growth lever. The merchants pulling ahead are not the ones with the most payment providers. They are the ones who decide, transaction by transaction, where each payment should go.

Most declines are not caused by the customer. They are caused by issuer behavior, routing inefficiencies, or processor performance. A valid card, sufficient funds, real intent to buy, and the transaction still fails because the path it took was not the right one. The same payment sent through a different acquirer would have gone through.

This is expensive in a way most teams never see, because the customer rarely complains. They just leave. False declines, legitimate purchases wrongly rejected, drain an estimated $443 billion from global e-commerce every year, more than thirteen times the cost of actual fraud.

That money is not lost to criminals. It is lost to routing decisions made badly in a few milliseconds, over and over.

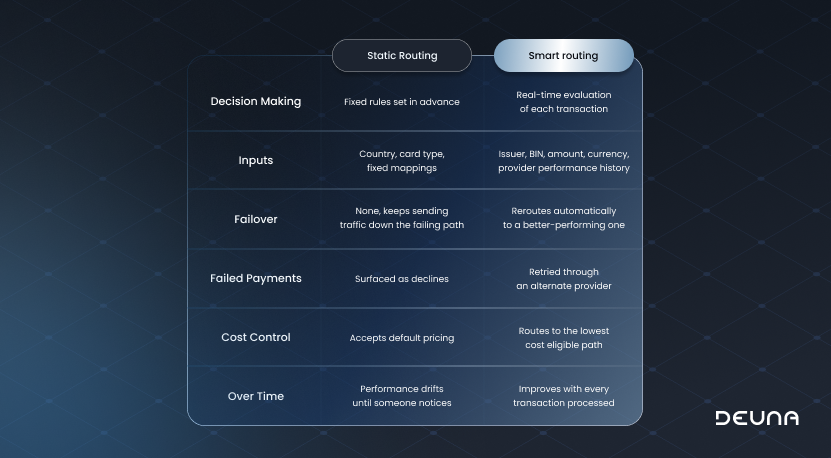

The fastest way to understand smart routing is to compare it to the fixed rules most stacks still run on.

"Smart routing" is not one thing. It is a set of specific tactics working together. Here is how the recovery actually happens.

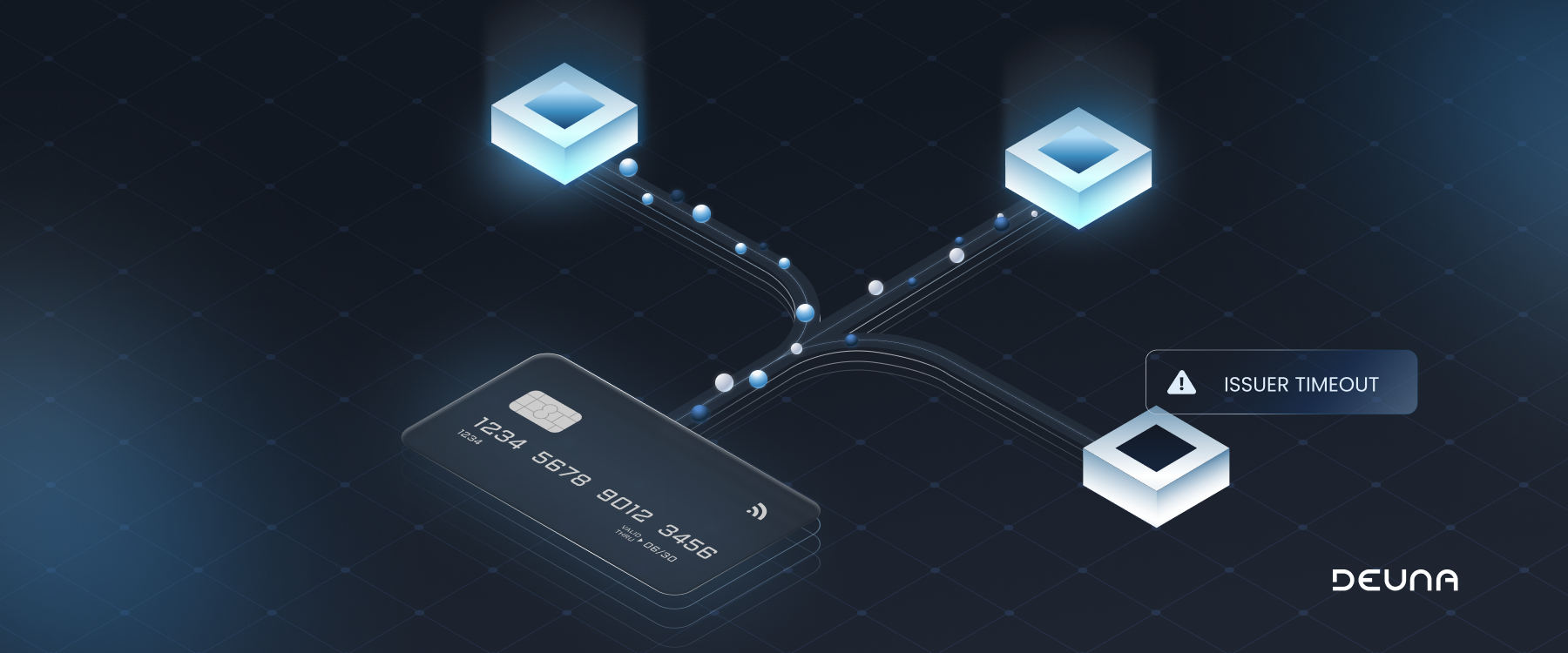

1. Intelligent retry on soft declines. Not every decline means stop. A soft decline, like an issuer timeout or a temporary network error, can succeed on a second attempt. Smart routing retries it automatically through an alternate provider so the customer never sees a failure. The trick is knowing which declines to retry, which leads to the next tactic.

2. Decline-code logic that separates recoverable from dead transactions. Retrying a hard decline wastes fees and can trigger fraud flags. Smart routing reads the decline reason and acts accordingly. Soft declines worth retrying include insufficient funds, an issuer or network that is temporarily unavailable, a processing timeout, or a velocity limit being hit. Hard declines like a stolen card, a closed account, or an invalid card number are dead ends and should never be retried.

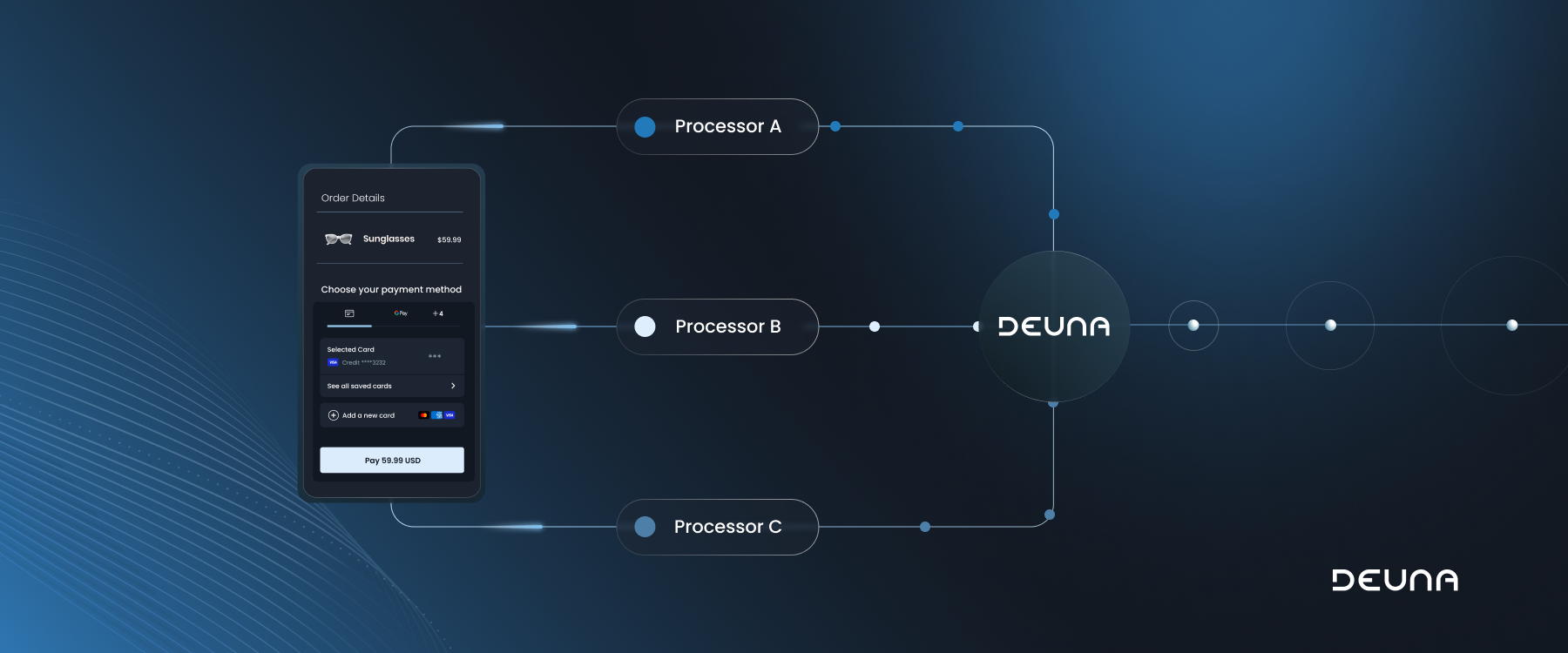

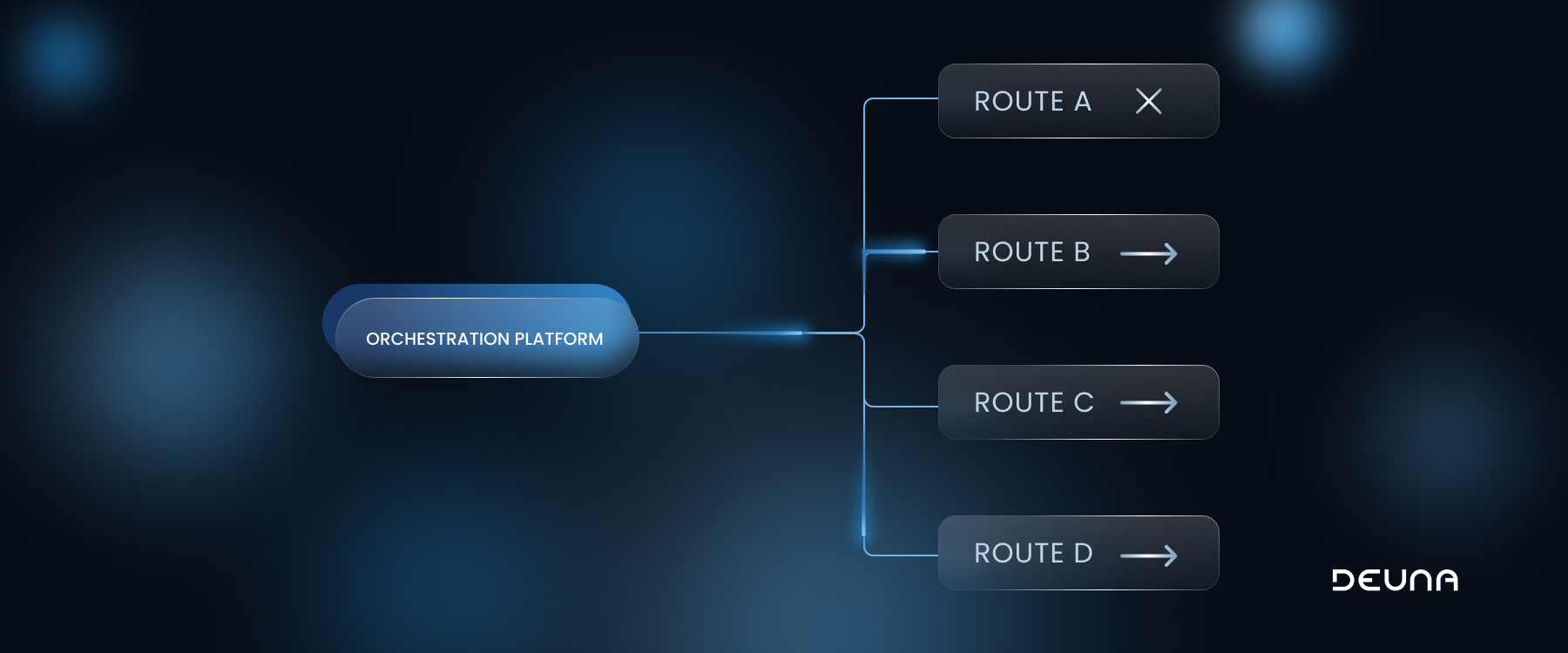

3. Cascading, or waterfall, routing. When the first-choice provider declines a recoverable transaction, the system passes it to the next-best provider in sequence, ranked by approval likelihood for that exact transaction type. One acquirer's "no" becomes another's "yes" without any friction for the shopper.

4. Network tokenization. Replacing raw card numbers with network tokens lifts approvals on its own. Visa reported a 6% improvement in approvals and a 30% reduction in fraud as token adoption climbed, and Fiserv found tokenized transactions see an average 2.1% authorization uplift over standard card numbers, with fraud rates declining 26%. Smart routing identifies

The tactics above are not one-time fixes. They get stronger when they feed each other. Approval rates, decline reasons, latency, and cost all become inputs that inform how the next transaction is routed, and over time that creates a system that improves with every payment processed. Instead of manually rewriting rules after a bad month, the routing adjusts on its own before the loss compounds.

That compounding is where the real gains live. A few points of acceptance uplift, a steady stream of recovered transactions month after month, lower fees on every path: none of it comes from a new product or a bigger marketing budget. It comes from making better decisions on payments the business is already receiving.

For years, the goal was access: connect more providers, accept more methods, cover more markets. That is now table stakes. The advantage today is not in how many providers you have. It is in how intelligently you use them.

Because in modern payments, success is no longer defined by access to multiple providers. It is defined by how intelligently you use them on every single transaction. Resilience is not redundancy. It is intelligence applied to each payment, in real time.